2017 Important Information for Employers, Pension Payers, and Others that Withhold North Carolina Income Tax

Issued By: Personal Taxes

Date: September 15, 2017

The following important information is addressed in this notice:

- Extension of automatic waiver of the requirement to file Form NC-3 electronically

- Penalty for failure to file Form NC-3 by January 31

- The repeal of the “Credit for Children” and the enactment of a new state tax deduction for children

- A change in the withholding rate for Tax Year 2019

During the 2015 session, the North Carolina General Assembly enacted Session Law 2015- 259 which changed the state’s withholding tax laws to increase tax compliance and help the Department combat tax refund fraud. As part of that legislation, G.S. 105-163.7 was amended to require employers, pension payers, and other persons that withhold North Carolina income tax to file Form NC-3, “Annual Withholding Reconciliation,” and the Department’s copies of W-2s, 1099s and other withholding statements on or before January 31 of the succeeding year in an electronic format as prescribed by the Secretary of Revenue. The statute also authorizes the Secretary, upon show of good cause, to waive the electronic submission requirement.

In 2015 and 2016, the Secretary granted an automatic waiver to businesses that could not meet the electronic submission filing requirement for NC-3s, W-2s, and 1099s due to be filed on January 31, 2016, and January 31, 2017, respectively. The Secretary has extended the automatic waiver for forms due to be filed on or before January 31, 2018. This is an automatic waiver – no action is required. This waiver, however, does not alleviate the business of its responsibility to timely file paper NC-3s, W-2 and 1099s.

Session Law 2015-259 also amended G.S. 105-236(a)(10)c to require the Department to assess a $50 penalty against an employer that fails to file an informational return with the Department by the date the return is due. The penalty was effective for taxable years beginning on or after January 1, 2016.

The Secretary elected to automatically waive the failure to file penalty on NC-3s due to be filed by January 31, 2017, but which were filed after that date. The Department will impose the failure to file penalty on NC-3s due to be filed on January 31, 2018 if the return is not timely filed.

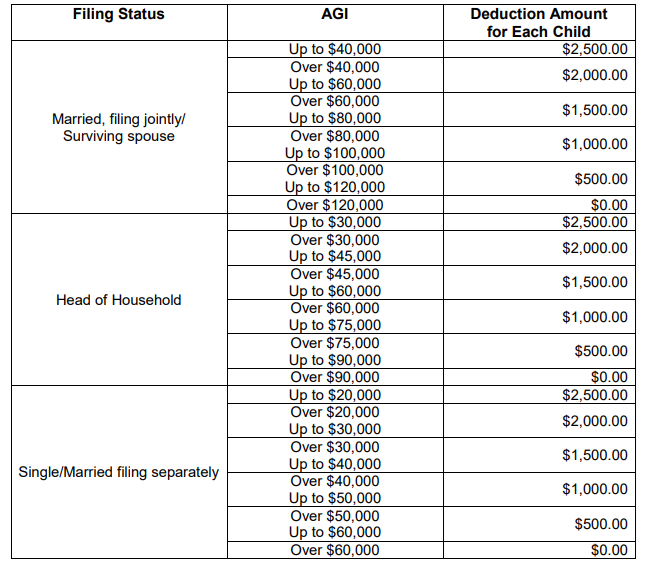

During the 2017 session, the North Carolina General Assembly enacted Session Law 2017-57 which converted North Carolina’s child tax credit to a child deduction. Prior to the enactment of this legislation, North Carolina law provided a taxpayer who was allowed a federal child tax credit with a North Carolina child tax credit of up to $125 per child, depending on a taxpayer’s filing status and amount of adjusted gross income. However, the child tax credit could not be used to reduce a taxpayer’s liability below zero. Therefore, if the taxpayer did not have a tax liability, then the tax credit did not benefit that person.

Effective for taxable years beginning on or after January 1, 2018, the “Credit for Children” has been repealed and replaced with a new “Child Deduction Amount.” New G.S. 105-153.5(a1) expands the number of taxpayers who may benefit by increasing the AGI limits and by providing five deduction amounts, as opposed to the current two credit amounts. The new “Child Deduction Amount” varies based on a taxpayer’s filing status and adjusted gross income (“AGI”) and is equal to the amount listed in the table below:

You are not required to obtain a new Form NC-4, NC-4EZ, or NC-4P from each employee or pension recipient because of the conversion of the child tax credit to a child deduction; however, be aware that an employee or pension recipient could either be entitled to an additional allowance or lose an existing allowance because of this law change. We request that you inform your employees or pension recipients of the repeal of the child tax credit and the enactment of the new child deduction and encourage them to review the number of allowances they claimed in 2017 to determine if the number should be adjusted.

Session Law 2017-57 also lowered the individual income tax rate from 5.499% to 5.25%. This change is effective for taxable years beginning on or after January 1, 2019. The withholding tables will be revised for 2019 to reflect the reduced tax rate. G.S. 105-163.2(b)(1) requires the withholding rate to equal the income tax rate plus one-tenth of one percent (0.1%). Therefore, the withholding tax rate for tax year 2019 will be 5.35%. The revised withholding tables for wages paid in 2019 will be included in Form NC-30 which will be available in late 2018.

This legislation also increased the standard deduction for each filing status. The change is effective for taxable years beginning on or after January 1, 2019, and will also be incorporated in the withholding tables for 2019.

As noted previously, you are not required to obtain a new Form NC-4, NC-4EZ, or Form NC-4P from each employee or pension recipient because of the tax rate reduction; however, be aware that an employee or pension recipient may be entitled to an additional allowance because of the reduced tax rate.

The Department uses its website as the primary resource for reporting law changes that affect withholding responsibilities. In addition, law changes will be explained in the Department’s annual Tax Law Changes publication, and in the annual revisions of withholding tax forms.

If you have any questions about this Important Notice, you may call 1-877-252-3052 to speak with a customer service representative or write to Customer Service, PO Box 1168, Raleigh, NC 27602.

To the extent there is any change to a statute or regulation, or new case law subsequent to the date of this notice, the provisions in this important notice may be superseded or voided. To the extent that any provisions in any other notice, directive, technical bulletin, or published guidance regarding the subject of this notice and issued prior to this notice conflict with this important notice, the provisions contained in this important notice supersede the previous guidance.