Impact of the American Rescue Plan Act of 2021 on the 2020 North Carolina Individual Income Tax Return

Issued By: Personal Taxes Division

Date: March 23, 2021 (Updated)

On March 11, 2021, the federal American Rescue Plan Act of 2021 (“ARPA”), was signed into law. The ARPA includes several coronavirus-related tax relief provisions, including a provision that makes the first $10,200 of 2020 unemployment benefits not subject to federal individual income tax for households with an adjusted gross income (“AGI”) of less than $150,000 per year. The exclusion applies to the first $10,200 of unemployment benefits for each spouse for married couples filing jointly. As of the date of this notice, North Carolina law has not incorporated any of the tax law changes enacted in the ARPA.

North Carolina General Statute (“N.C. Gen. Stat.”) § 105-153.7(a) provides that “a tax is imposed for each taxable year on the North Carolina taxable income of every individual.”

N.C. Gen. Stat. § 105-153.4 provides that for individuals who are residents of this state, nonresidents of this state, or part-year residents of this state, the term “North Carolina taxable income” refers to “the taxpayer’s adjusted gross income” as modified in N.C. Gen. Stat. §§ 105-153.5 and 105-153.6.

N.C. Gen. Stat. § 105-153.3(1) provides that “adjusted gross income” is the taxpayer’s federal adjusted gross income as defined in section 62 of the Code.”

N.C. Gen. Stat. § 105-228.90(b)(7) defines the term “Code” as “the Internal Revenue Code as enacted as of May 1, 2020, including any provisions enacted as of that date that become effective either before or after that date.”

For individual income tax purposes, the starting point for determining North Carolina taxable income is AGI as defined in the Internal Revenue Code (“Code”) as of a certain date. North Carolina currently references the Code as of May 1, 2020.

Because North Carolina’s individual income tax law incorporates by reference many of the provisions of the Code as of a specific date, the General Assembly must determine whether to update the state’s reference to the Code. Importantly, unless the General Assembly updates North Carolina law to reference the Code as it was enacted as of March 11, 2021, or later, the tax provisions in the ARPA, including the provision to excluded a portion of unemployment compensation from AGI, do not apply to an individual when calculating North Carolina taxable income for tax year 2020.

The 2021 session of the General Assembly is currently underway. Even if the General Assembly enacts legislation to update the State’s reference to the Code to March 11, 2021, or later, the General Assembly may choose not to adopt all of the tax provisions included in the ARPA, including the retroactive provision that makes the first $10,200 of 2020 unemployment benefits nontaxable.

Taxpayers who file their 2020 Form D-400 prior to any action of the General Assembly and whose AGI excludes unemployment compensation pursuant to the provisions of the ARPA must add back the amount of unemployment compensation excluded from AGI when determining North Carolina taxable income.

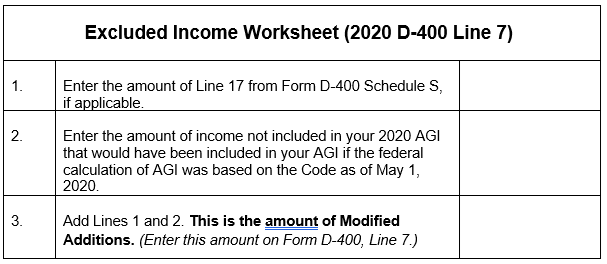

Resident taxpayers must first complete Form D-400 Schedule S, Part A for tax year 2020. Next, add the amount of Form D-400 Schedule S, Line 17, Total Additions, to the amount of unemployment compensation excluded from AGI to calculate the amount of modified additions for tax year 2020 (“Modified Additions”). The amount of Modified Additions must be entered on Form D-400, Line 7, Additions to Federal Adjusted Gross Income. (See the Unemployment Compensation Worksheet below.)

In addition to the above, part-year resident or nonresident taxpayers who are required to file Form D-400, PN for tax year 2020 must also enter the full amount of unemployment compensation received in 2020 on Form D-400 PN, Column A, Line 13, Unemployment Compensation. In Column B, enter the amount of Column A that is applicable to North Carolina. Do not reduce the amount of Line 13, Column A or Column B, by the amount of unemployment compensation excluded from federal income. Importantly, part-year resident or nonresident taxpayers must not reduce Form D-400 PN, Line 15, Column A or B, Other Income, by the amount of unemployment compensation excluded from federal income.

Taxpayers may choose to wait to file their 2020 Form D-400 until after the General Assembly enacts legislation updating the state’s reference to the Code. A taxpayer who files a 2020 Form D-400 after the original due date of the return must be granted an extension of time to file the state income tax return. Without a valid extension, a 2020 Form D-400 filed after the due date of the original return is delinquent. Importantly, an extension of time to file a tax return does not extend the time to pay the tax due. If you do not pay the amount of tax due by the original due date, you may owe additional penalties and interest as provided by law.

If the General Assembly subsequently adopts the federal tax treatment of unemployment compensation for tax year 2020, taxpayers who filed their 2020 Form D-400 prior to the actions of the General Assembly and who included unemployment benefits not subject to federal tax in the calculation of state taxable income may file an amended Form D-400 to request a refund of any overpaid tax.

If you have any questions about this notice, you may call the North Carolina Department of Revenue Customer Service line at 1-877-252-3052 (8:00 a.m. until 5:00 p.m. EST, Monday through Friday), or write to Customer Service, PO Box 1168, Raleigh, NC 27602.

To the extent there is any change to a statute or regulation, or new case law subsequent to the date of this notice, the provisions in this important notice may be superseded or voided. To the extent that any provisions in any other notice, directive, technical bulletin, or published guidance regarding the subject of this notice and issued prior to this notice conflict with this important notice, the provisions contained in this important notice supersede the previous guidance.