Sales and Use Tax Directive 24-2

Maximum Use Tax on Purchases of Qualifying Spirituous Liquor

Tax: Sales and Use Tax

Law: Session Law 2024-41, Section 23

Issued By: Sales and Use Tax Division

Date: December 17, 2024

Number: SD-24-2

This directive provides the interpretation of the Secretary of Revenue regarding the maximum use tax on purchases of qualifying spirituous liquor.

The following important information is addressed in this directive:

- Overview of Qualifying Spirituous Liquor

- Maximum Tax on Purchases of Qualifying Spirituous Liquor

- How to Purchase Qualifying Spirituous Liquor with Direct Pay Permit

- How A Seller Can Elect to Collect the Maximum Tax

- Examples

For the purposes of this directive, “qualifying spirituous liquor” means a single container of spirituous liquor, as defined in N.C. Gen. Stat. § 18B-101, the purchase price of which is equal to or greater than fifty thousand dollars ($50,000).

Examples of a single container of spiritous liquor include:

- A single 0.75 liter, closed bottle of brandy.

- A single 1.75 liter closed bottle of bourbon.

- A single 700 milliliter closed can of premixed cocktail sold by someone other than a mixed beverage permittee.

Effective January 1, 2025, certain purchases of qualifying spirituous liquor are subject to a maximum $1,000 tax.1 For a purchase to be subject to the maximum tax, the purchaser must obtain a Qualifying Spiritous Liquor Direct Pay Permit or the retailer must elect to collect the maximum tax.

Step 1 - Obtain A Direct Pay Permit

A person must apply for a Qualifying Spiritous Liquor Direct Pay Permit. To apply, the person must submit a completed Form E-595SL, Application Direct Pay Permit for Qualifying Spirituous Liquor.

If approved, the Department will issue a Qualifying Spirituous Liquor Direct Pay Permit that includes a direct pay number.

Step 2 – Provide the Seller Exemption Documentation

To purchase qualifying spirituous liquor without paying tax to the seller, the purchaser must provide the seller one of the following (collectively “Direct Pay Documentation”):

- A copy of the Direct Pay Permit (paper or digital);

- Completed Form E-595E, Streamlined Sales and Use Tax Agreement Certificate of Exemption (“Exemption Certificate”); or

- Electronically provide the required data elements1 for an Exemption Certificate.

If providing an Exemption Certificate or electronically providing the data elements, the purchaser must identify the reason for the exemption as a direct pay permit and provide their direct pay number.

If a purchaser provides a seller Direct Pay Documentation at the time of sale, the seller should exempt the sale from sales and use tax. The seller should report the sale on Line 1, “Gross Receipts or Sales” and Line 3, “Exempt Gross Receipts or Sales” on Form E-500E, Combined General Rate Sales and Use Tax Return (Utility, Liquor, Gas, and Other) (“Form E-500E”).

Step 3 – Purchaser Must Report and Pay Use Tax to the Department

A person who purchases qualifying spirituous liquor using a direct pay permit must file and pay use tax directly to the Department using Form E-500E. The tax must be paid by the 20th of the month following the month of purchase. The purchaser must pay $1,000 of use tax for each qualifying spiritous liquor purchase.

Form E-500E is available for download on the Department’s website. The purchaser must follow the instructions on the form with the following changes:

- Demographic Information - Enter the purchaser’s name and address as it appears on the Qualifying Spirituous Liquor Direct Pay Permit. For the “Period Beginning” and “Period Ending” fields, enter the date of the first and last day of the month of purchase. In the “Account ID” field, enter “Applied”.

- Line 1, Gross Receipts or Sales for Resale - Enter the total purchase price of the qualifying spirituous liquor.

- Line 3, Exempt Gross Receipts or Sales - Enter the amount of the purchase price of each qualifying spiritous liquor purchase that exceeds $14,285.71. To calculate this amount, the permit holder should reduce the purchase price of each qualifying spirituous liquor purchase by $14,285.71 and report that total difference.

- Line 9, Spirituous Liquor under the Receipts and Purchases column - Compute the purchase price subject to tax by multiplying the number of bottles of qualifying spirituous liquor purchased by $14,285.71 and enter the amount under Receipts and Purchases.

- Attachment - Attach a copy of the Qualifying Spirituous Liquor Direct Pay Permit.

- Filing the Return - Mail the return, payment, and attached Qualifying Spirituous Liquor Direct Pay Permit to:

- North Carolina Department of Revenue

- Attention: Registration Unit

- Post Office Box 25000

- Raleigh, North Carolina 27640-0001

- 1

Required data elements include purchaser's name, address, sales and use tax identification number or other North Carolina issued exemption number, type of business, reason for exemption, and signature if provided in paper format. The retailer must maintain this information in a retrievable format in its records.

Instead of requiring purchasers to obtain a direct pay permit, a seller can elect to collect the maximum use tax for qualifying spiritous liquor. If a seller makes this election, the seller must charge its customers the maximum tax of $1,000 for each sale of qualifying spiritous liquor. The seller must provide its purchasers an invoice that shows the tax collected on the purchase.

If a seller elects to collect the maximum tax, the seller must report sales of qualifying spirituous liquor on Form E-500E. The seller must follow the instructions on the form with the following changes:

- Line 3, Exempt Gross Receipts or Sales - Enter the total receipts reported on Line 1 of Form E-500E that are exempt from tax including the portion of each sale of qualifying spiritous liquor that exceeds $14,285.71. To calculate this amount, the seller should reduce the sales price of each qualifying spirituous liquor sale by $14,285.71 and report that total difference.

- Line 9, Spirituous Liquor under the Receipts and Purchases column - For sales of qualifying spiritous liquor, compute the receipts subject to tax by multiplying the number of bottles of qualifying spirituous liquor sold by $14,285.71. Add this amount to the other receipts and purchases of spiritous liquor subject to tax.

If a seller makes this election, the customer will pay the maximum tax directly to the seller. The purchaser should not apply for a direct pay permit and should not file Form E-500E for the purchase.

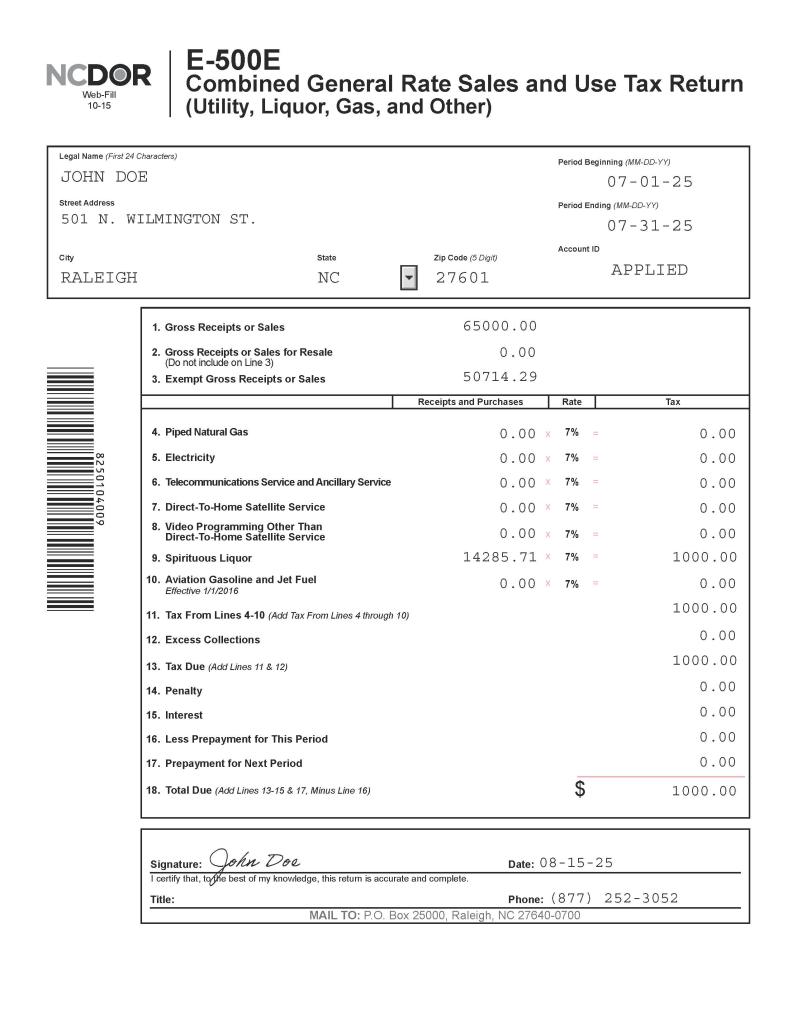

Example 1:

On July 3, 2025, John Doe purchases a bottle of spiritous liquor for $65,000 from a retailer located in North Carolina. The single container of spirituous liquor is qualifying spiritous liquor. Prior to the purchase, John Doe applied for and received a Qualifying Spirituous Liquor Direct Pay Permit. John Doe brings the Qualifying Spirituous Liquor Direct Pay Permit and completed Form E-595E to the retailer. John Doe entered the direct pay permit number issued by the Department for letter “J Direct pay permit #” under “4 Reason for exemption” on the exemption certificate. John Doe provides the completed E-595E to the retailer.

The retailer does not charge the customer any sales or use tax on the sale of qualifying spiritous liquor. The retailer keeps a record of the sale to John Doe and the exemption certificate in its records. The retailer treats the sales as exempt from sales and use tax and reports the entire purchase price of $65,000 on Lines 1 and 3 of its Form E-500E for July 2025 due on or before August 20th.

On August 15, 2025, John Doe completes Form E-500E. When filing Form E-500E, John Doe enters the purchase price of $65,000 on Line 1. John Doe calculates the amount to report on Line 3 by reducing the $65,000 purchase price by $14,285.71 which equals $50,714.29 ($65,000 - $14,285.71 = $50,714.29). John Doe enters $50,714.29 on Line 3. John Doe reports $14,285.71 on Line 9 under the Receipts and Purchases column. The purchase price reported on Line 9 is multiplied by the 7% tax rate to calculate the amount of tax to report of $1,000 ($14,285.71 x 7%= $1,000). John Doe enters $1,000 on Line 9 under the Tax column. John Doe completes the rest of Form E-500E according to the form’s instructions. Finally, John Doe mails the return, payment, and direct pay permit to the address listed above.

Example 2:

Jane Doe purchases an auction lot that consists of 2 containers of spiritous liquor for $101,000 which includes the buyer’s premium at an auction in North Carolina. The sale is not of a sale of qualifying spiritous liquor because it is not the sale of a single container of spirituous liquor. The entire sales price of $101,000 is subject to the 7% combined general rate of sales and use tax and must be collected and reported by the retailer on its sale.

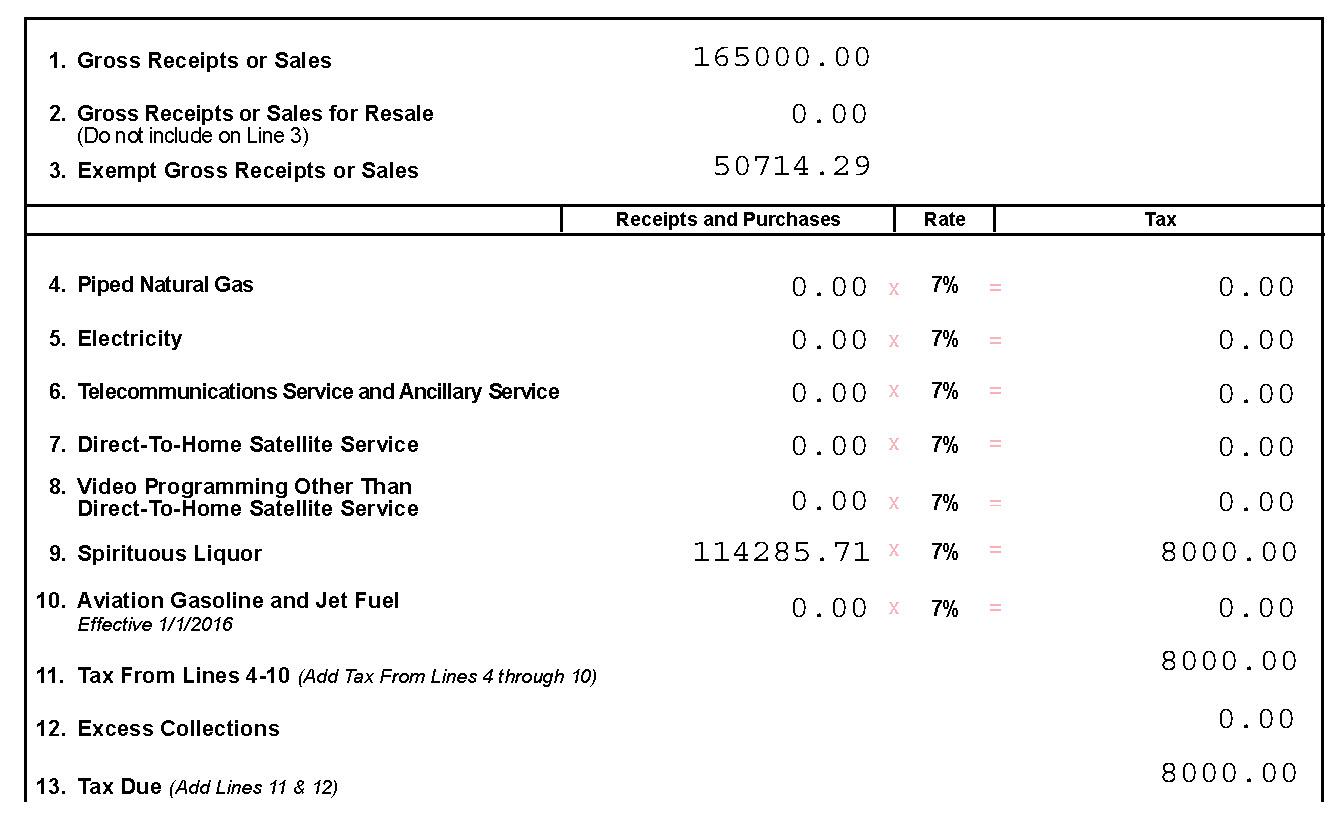

Example 3:

John Doe purchases a bottle of spiritous liquor for $65,000 at Distiller in North Carolina. The single container of spirituous liquor is qualifying spiritous liquor. Distiller elects to collect and remit the maximum amount of tax on the qualifying spirituous liquor. Distiller generates an invoice for the purchaser that shows the purchaser paid the $1,000 tax on the purchase.

In addition to the purchase by John Doe, Distiller sells $100,000 of spiritous liquor that is not qualifying spiritous liquor to other customers.

When Distiller reports the sale of the qualifying spirituous liquor on its Form E-500E, Distiller enters its total gross sales of $165,000 on Line 1 ($100,000 + $65,000 = $165,000). Distiller calculates the amount to report on Line 3 by reducing the $65,000 sales price by $14,285.71 which equals $50,714.29 ($65,000 - $14,285.71 = $50,714.29). Distiller enters the difference of $50,714.29 on Line 3. Next, Distiller multiplies the number of bottles of qualifying spiritous liquor sold by $14,285.71 and adds that amount to its other receipts (1 x $14,285.71 + $100,000 = $114,285.71). Distiller enters that amount on Line 9 under the Receipts and Purchases column. Finally, the retailer will complete the rest of Form E-500E according to the form’s instructions.

Assistance

If you have questions about this directive, you may call the Department at 1-877-252-3052 (8:00 a.m. until 4:30 p.m. EST, Monday through Friday).

To the extent there is any change in the rate or amount of tax, change to a statute or regulation, or new case law subsequent to the date of this directive, the provisions in this directive may be superseded or voided. To the extent that any provisions in any other notice, directive, bulletin, or published guidance regarding the subject of this directive and issued prior to the date of this directive conflict with this directive, the provisions contained in this directive supersede the previous guidance.